The Construction Products Association (CPA) has downgraded its forecast for this year and next. They expect construction output to fall by 7% this year.

The forecast was 6.4% at the start of May, with only a modest increase in 2024 of 0.7%. The forecast is based on the Bank of England interest rate peaking at 5.75% in 2023 Q4, but as material supply stabilises and economic data is released, this will have an impact.

By far the biggest fall in construction output is in private housing, which is forecast to fall by 19% this year, with only a modest 2% increase in 2024. The slow down is partially blamed on high interest rates which is subduing demand for new homes. Despite the downturn in the UK construction forecast, CAB members remain fairly busy and optimistic despite uncertain times ahead.

The rate at which clients decide to enter into new construction contracts has slowed. Whilst there is a lot of construction in the pipeline, there is doubt about how quickly this will translate into starts on site.

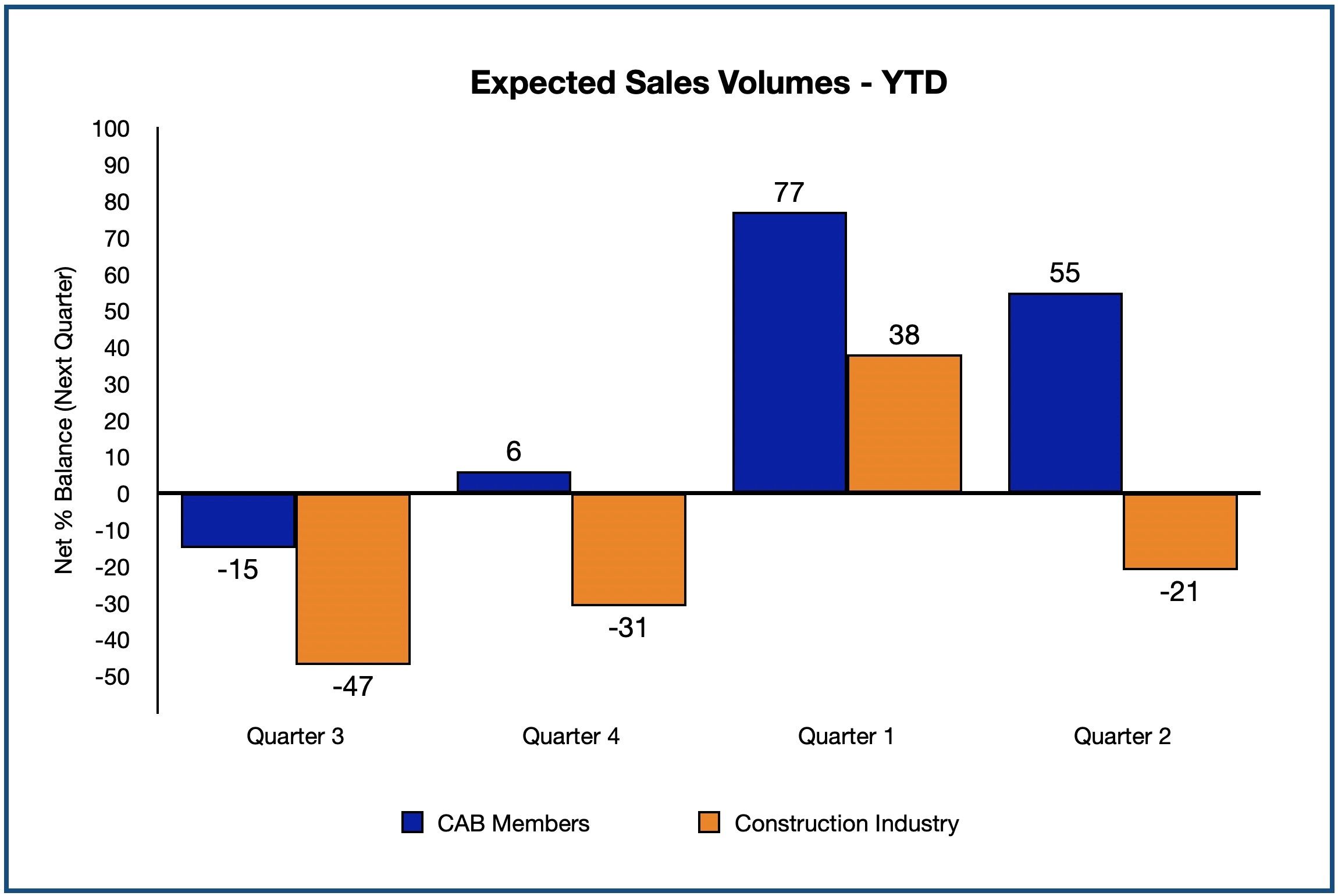

On net balance, 45% of CAB members have seen historic sales volumes increase. This is in contrast to the wider construction industry, which reported a -47% reduction in sales over the same period.

On net balance, 45% of CAB members have seen historic sales volumes increase. This is in contrast to the wider construction industry, which reported a -47% reduction in sales over the same period.

Historic sales volumes in the year to date show a continuous increase. The wider construction industry’s values have dipped considerably compared to Q1 2023 (just -7% on net balance of respondents).

Following a good start to the year where CAB members forecast an increase in sales of 77% in the first quarter, this has softened a little to 55%. Slowing in the wider construction market brings down the forecasts of CAB members. Large variation between the two markets could suggest volatility ahead.

Although material supply has recovered well since the height of the Covid-19 pandemic, financial aspects (borrowing and the increasing cost of materials) are bringing about instability and could create uncertainty for many businesses in the latter part of the year.

Quarter-on-quarter sales volume figures for CAB members show a healthy increase. Only 9% of firms report a decrease of less than 5%. More than half (54%) indicated an increase in sales over Q1 2023; 36% reported an increase over 5%.

Historically, as new build slows, refurbishment increases. As can be seen in previous downturns, aluminium fenestration is quick to transfer into refurbishment from new build, as building owners turn to put a new face onto existing property. This work is quicker coming through the pipeline.

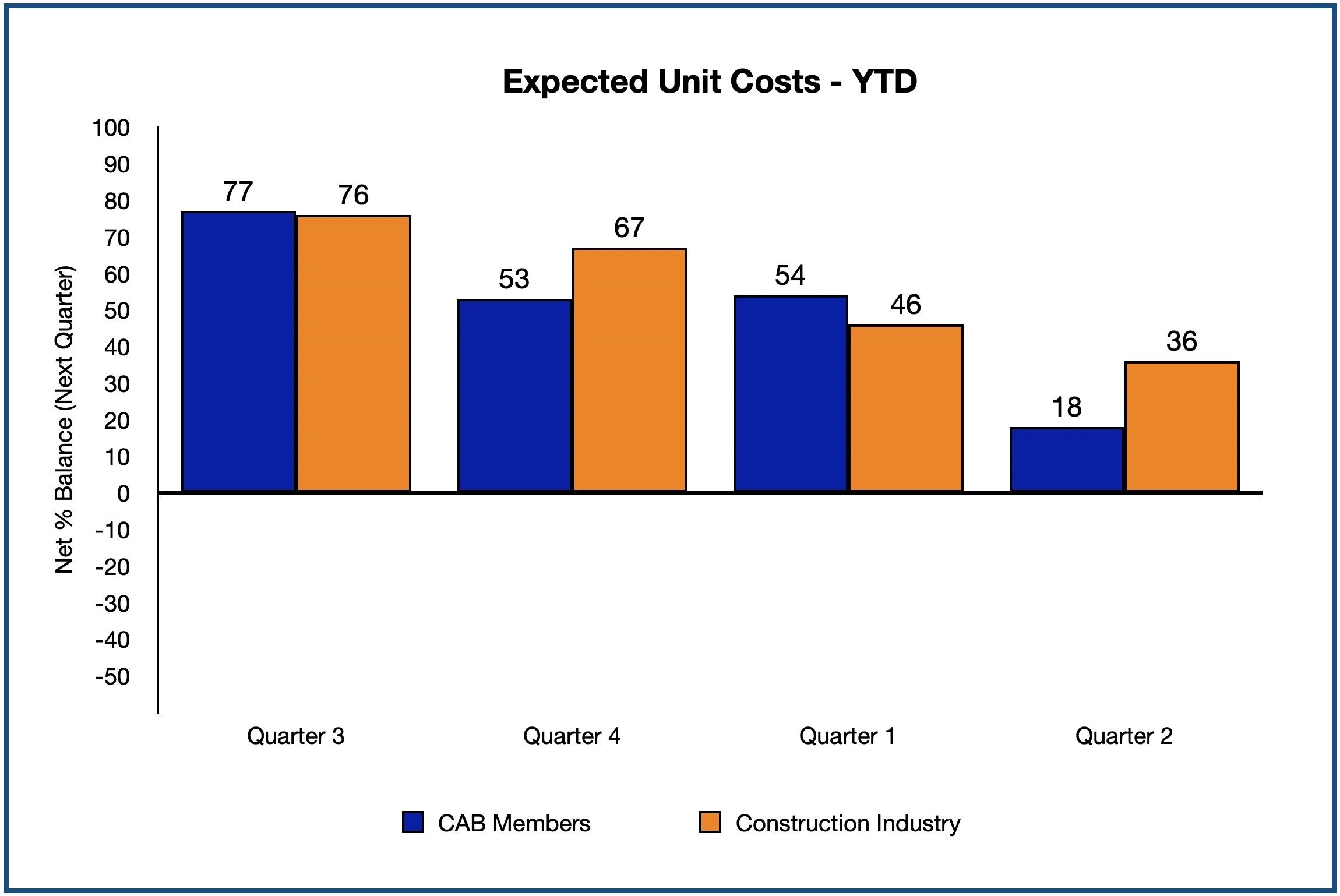

The trend on historic and expected unit costs has softened over the last year across the construction industry. Aluminium prices have reduced by 15% since a high early in the year, however hardware and other materials continue to have an impact.

The trend on historic and expected unit costs has softened over the last year across the construction industry. Aluminium prices have reduced by 15% since a high early in the year, however hardware and other materials continue to have an impact.

CAB members report that wages and salaries are now the major cost factor. Energy costs as a cost factor has softened to 64% from a year ago where the proportion was 100%. From a high of 78% in Q4 2022, no respondents indicated that raw materials were a cost factor in Q2 2023.

Looking forward, CAB members claim that the likely constrain on activity over the next 12 months remains demand: 82% of respondents claim this as the major factor. This has remained steady over the last year. Labour availability is the second constant, as 9% of respondents claim this as a constraint over the next 12 months.

CAB members’ capital investment in plant equipment and product improvement has always remained high. In Q2 2023 emphasis has now moved to product improvement. The challenge to meet higher thermal performance levels in order to meet future legislation is clearly a driving factor.

The full report, which places CAB members’ feedback against the wider construction products sector, produced by the CPA, is a members-only document. This, together with other market data, forms part of the support package for CAB members. To learn more about, contact CAB directly, or consider joining the association. Information can be found on our website.

Phil Slinger

CEO of the Council for Aluminium in Building (CAB)